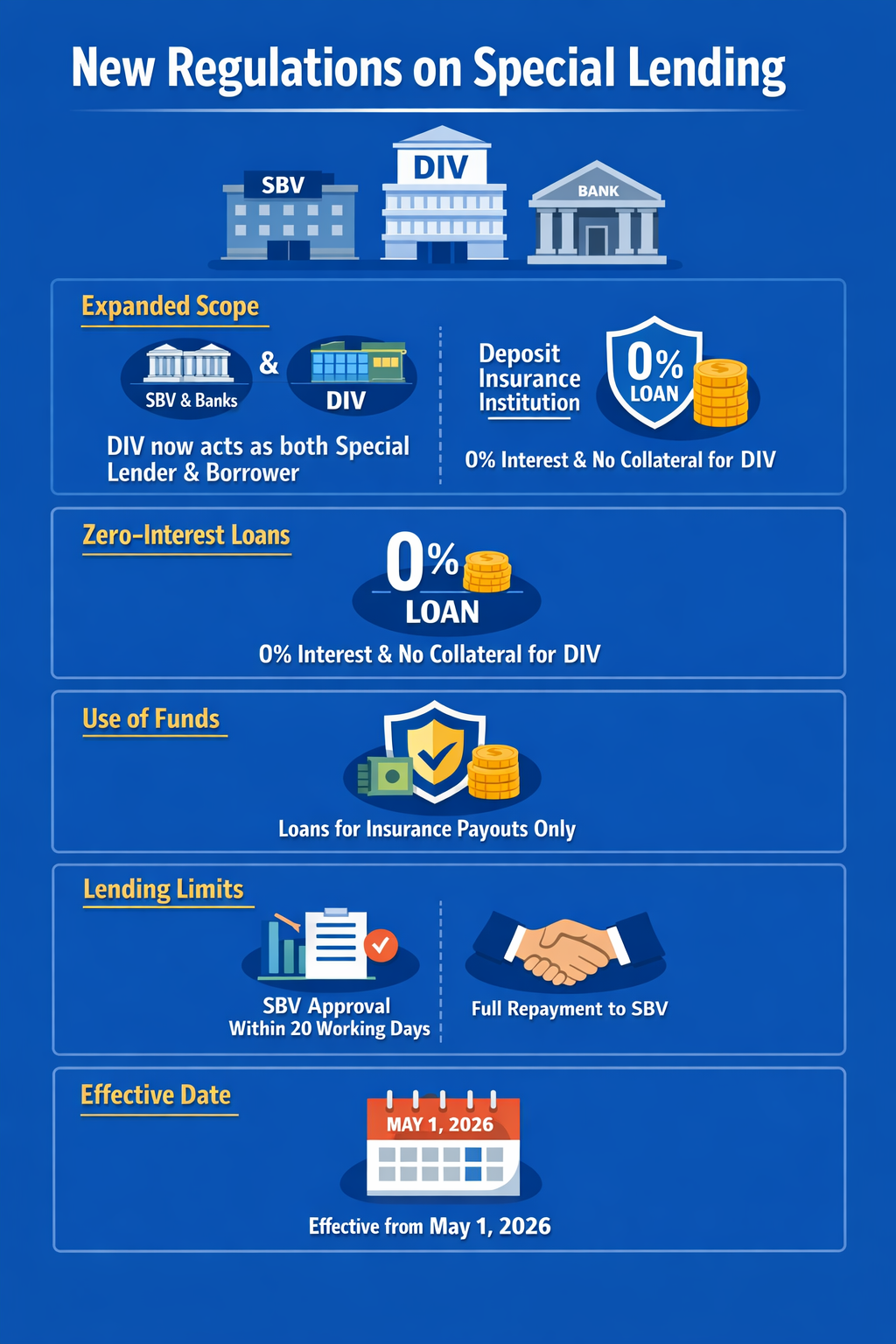

Expanded scope and participating entities

The Circular broadens the scope of applicable entities, explicitly including the Deposit Insurance of Vietnam (DIV) and other relevant organizations and individuals involved in special lending activities. This marks a notable development, positioning the deposit insurance institution as a formal participant in the special lending mechanism alongside the SBV and credit institutions.

A key highlight is the establishment of a dual role for the deposit insurance institution. Under the new provisions:

- It may act as a special lender, together with the SBV and other credit institutions; and

- It may also act as a borrower, obtaining special loans from the SBV.

This design enhances flexibility in the mechanism, enabling broader participation to support liquidity stress within the financial system.

Zero-interest, unsecured lending for deposit insurance institution

Notably, the Circular introduces provisions for special loans at a 0% annual interest rate without collateral for the deposit insurance institution in cases stipulated by law.

This preferential mechanism allows the institution to mobilize additional resources to fulfill its mandate, particularly in reimbursing insured deposits when necessary.

Conversely, the deposit insurance institution is also authorized to provide special loans to credit institutions using its professional reserve fund, thereby strengthening systemic support tools.

Use of funds and lending limits

The Circular clearly stipulates that:

- Special loans obtained by the deposit insurance institution must be used exclusively for insurance payouts.

- The loan amount is determined based on actual funding needs and must not exceed the shortfall in the institution’s reserve fund.

Interest rate policy

The preferential policy is reaffirmed:

- The interest rate on the principal of special loans is 0% per annum.

- No interest is charged on overdue interest.

This underscores the emergency and supportive nature of special lending, aimed at addressing urgent liquidity needs without increasing financial burdens.

Procedures and approval process

The Circular establishes a stringent process for borrowing, disbursement, and repayment:

- The deposit insurance institution must submit a comprehensive application dossier to the SBV, specifying the loan amount, purpose, term, and commitment to proper use of funds.

- Within a maximum of 20 working days from receipt of a complete dossier, the SBV Governor will review and decide on the loan approval.

Repayment obligations and enforcement

Upon maturity:

- The deposit insurance institution is required to fully repay the loan to the SBV.

- In cases of non-compliance or misuse of funds, the SBV may take enforcement actions, including debiting the institution’s accounts to recover the loan.

Responsibilities of relevant parties

The Circular also clarifies the responsibilities of stakeholders:

- The deposit insurance institution must provide accurate information, use funds appropriately, and comply with legal regulations.

- Relevant units within the SBV are tasked with coordination, supervision, and handling violations.

Effective date and policy objective

Circular No. 02/2026/TT-NHNN will take effect on May 1, 2026.

Its issuance aims to:

- Implement provisions of the 2025 Law on Deposit Insurance; and

- Further strengthen the legal framework for special lending, thereby enhancing the capacity to support and safeguard the stability of the banking system.

VGP/VNBA News